A few weeks after Amazon spent $1B buying the live video game streaming platform Twitch, ESPN president John Skipper was asked for his thoughts on the burgeoning “eSports” opportunity. “It’s not a sport — it’s a competition,” he responded, “Chess is a competition. Checkers is a competition… Mostly, I’m interested in doing real sports.”

This type of ostracizing skepticism isn’t new to sports. A similar distinction was made by industry executives, sportscasters and sports fans when “extreme sports” started receiving press coverage in the early 1990s. In fact, many of the same arguments have been repurposed, such as the claim that “real” sports require innumerable hours of intense mental and physical training. Today, however, few still question the legitimacy of extreme events or their athletes. This year, ESPN will host its 20th annual Summer X-Games and 17th annual Winter X-Games, each of which will draw between 30 and 40 million US viewers. What’s more, eight of the 12 new events at the 2014 Sochi Winter Olympics began at the X-Games.

eSports, too, are rapidly developing. Professional players now practice 8 to 12 hours each day just to stay on the top of their game and invest much of their remaining time researching the techniques and styles of their competitors. Those looking to be title contenders hire expert coaches to lead them through rigorous training programs and perform the type of post-game analysis that matches even the most technical of NFL players. “You’re literally sacrificing your [youth] to become a professional gamer,” former World Tour Champion Johnathan Wendel told the Kernel last year. “You have to sacrifice time, time with family, time with everyone. You’re focusing on yourself on becoming a better player at all times… [else] you’re not going to be the best in the world.” For these players, being the best means joining leagues, or trying out for/being traded to (or benched on) professional teams, and most notably, joining the tournament circuit. eSports tournaments, in fact, may be the best representation of the industry’s newfound prominence. Though once relegated to basements and warehouses, these events are proliferating across the globe and building audiences that can reach tens of millions.

Last year’s League of Legends championship, for example, drew nearly 30 million viewers, putting it in line with the combined viewership of the 2014 MLB and NBA finals, or the series finales of Breaking Bad and Two and a Half Men, plus the Season 4 finale of Game of Thrones. As with most sports, competitive gaming is now firmly entrenched in the US college system, with the country’s largest collegiate league counting more than 10,000 active players, some of whom are on full athletic scholarships. Eager to capitalize on growing interest in the sport, Major League Gaming (MLG) opened the first dedicated domestic eSports arena in October 2014, and major brands such as Ford, American Express and Coke have begun forming partnerships with game developers, teams, players, event organizers and video distributors. The US Department of State has been issuing athlete visas to competitive gamers since 2013.

Last year’s League of Legends championship, for example, drew nearly 30 million viewers, putting it in line with the combined viewership of the 2014 MLB and NBA finals, or the series finales of Breaking Bad and Two and a Half Men, plus the Season 4 finale of Game of Thrones. As with most sports, competitive gaming is now firmly entrenched in the US college system, with the country’s largest collegiate league counting more than 10,000 active players, some of whom are on full athletic scholarships. Eager to capitalize on growing interest in the sport, Major League Gaming (MLG) opened the first dedicated domestic eSports arena in October 2014, and major brands such as Ford, American Express and Coke have begun forming partnerships with game developers, teams, players, event organizers and video distributors. The US Department of State has been issuing athlete visas to competitive gamers since 2013.

It’s becoming increasingly difficult to say eSports aren’t “real” sports, but the bigger question is whether it even matters. The media business is about eyeballs, and audiences are turning up in droves for the likes of Defense of the Ancients and League of Legends. Any media company looking to protect or establish an empire would be foolish to look down on such an opportunity, however arcane.

The Perfect Audience?

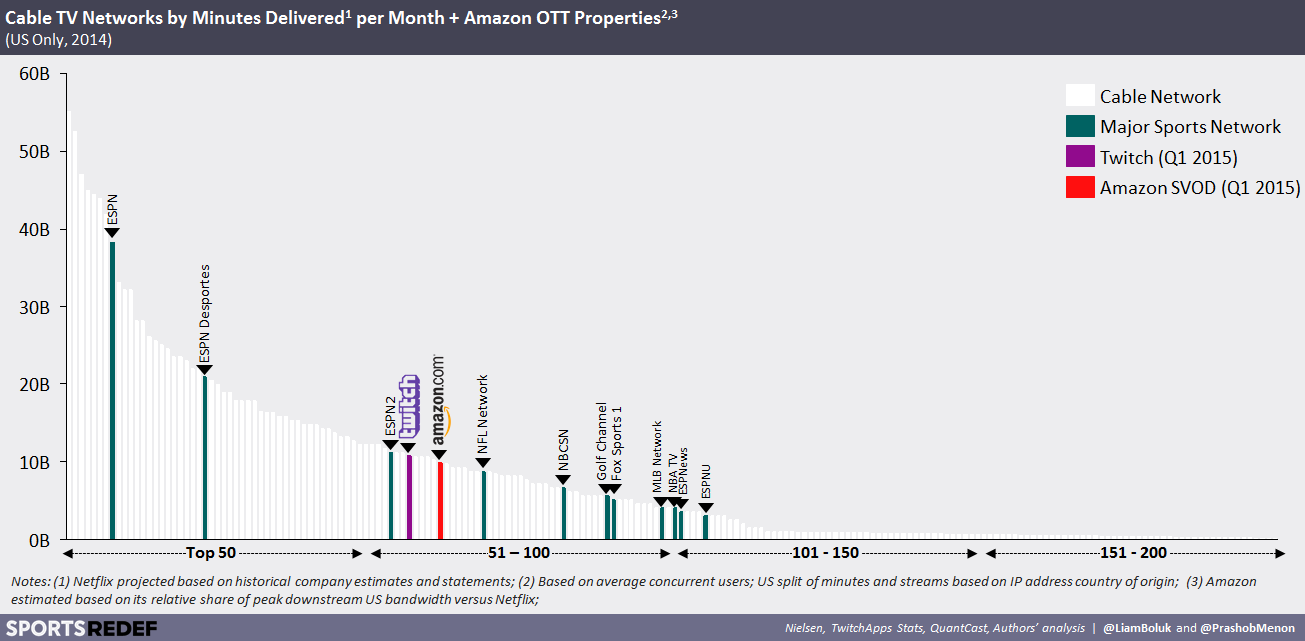

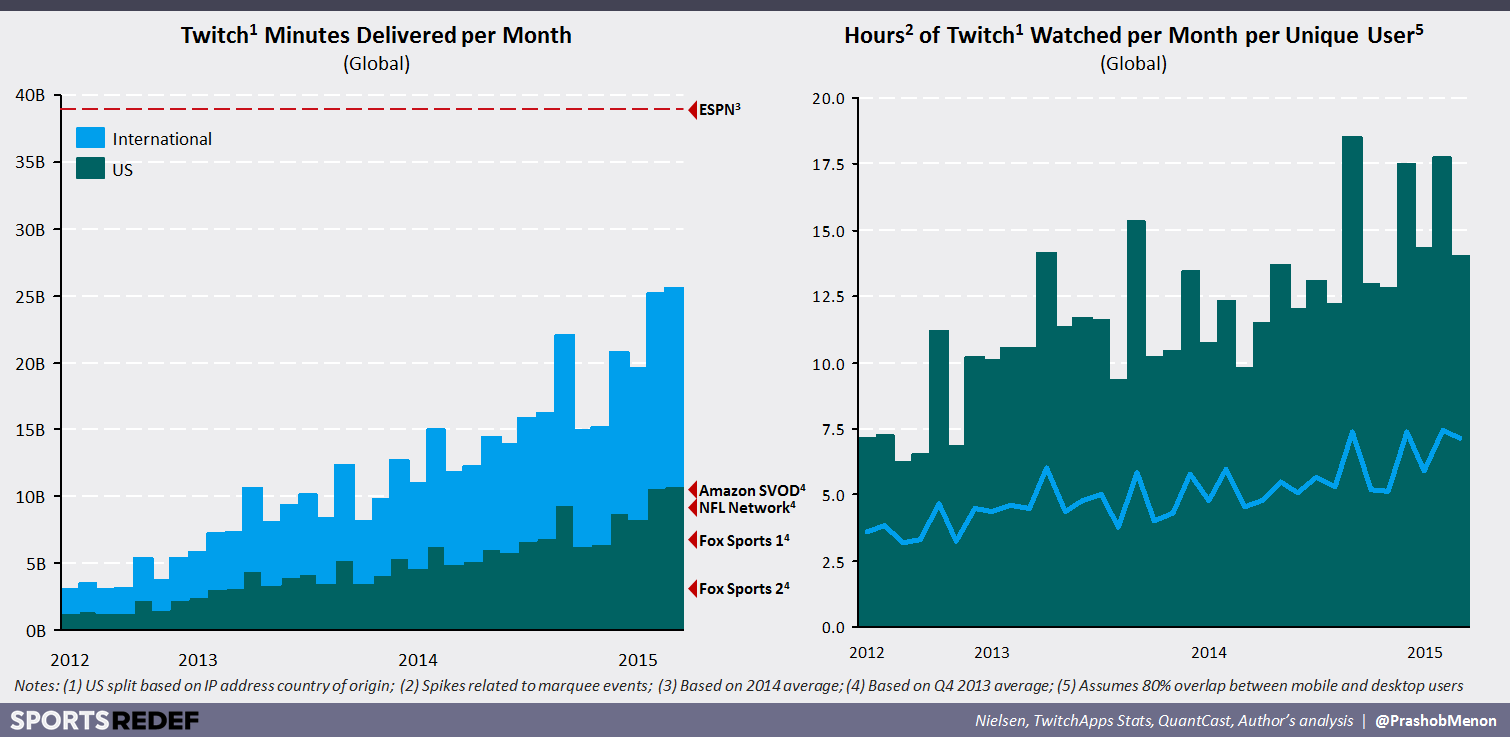

Though the eSports narrative tends to focus on the industry’s marquee tournaments and events, this overlooks the ways in which the genre has integrated itself into the daily lives of millions worldwide. In March 2015, Twitch averaged more than 600,000 simultaneous viewers, reached an audience of 51M worldwide and delivered more than 26B minutes of video entertainment. On a domestic basis, 11B minutes were watched in March – representing roughly 14 hours for each of the 13M American viewers. This consumption is so great that Twitch is already larger than 70% of American television networks, as well as Amazon’s own OTT video service.

However, the value of this consumption isn’t just its magnitude. An estimated 70% of all viewers are under the age of 35, making Twitch’s audience both highly valuable to advertisers and hard to reach via traditional television. Moreover, eSports fans, unlike linear TV viewers, are highly engaged in the content. Major League Gaming, for instance, consistently beats the industry average on key digital ad metrics such as completion rates (90% vs. 72%), click-through rates (4% vs. 2%), and ad viewability (99% vs. 44%). What’s more, Twitch shows little sign of slowing down. Total minutes delivered (both domestic and abroad) have grown by an average of 7% each month for the past three years, while per viewer consumption has doubled over that same period.

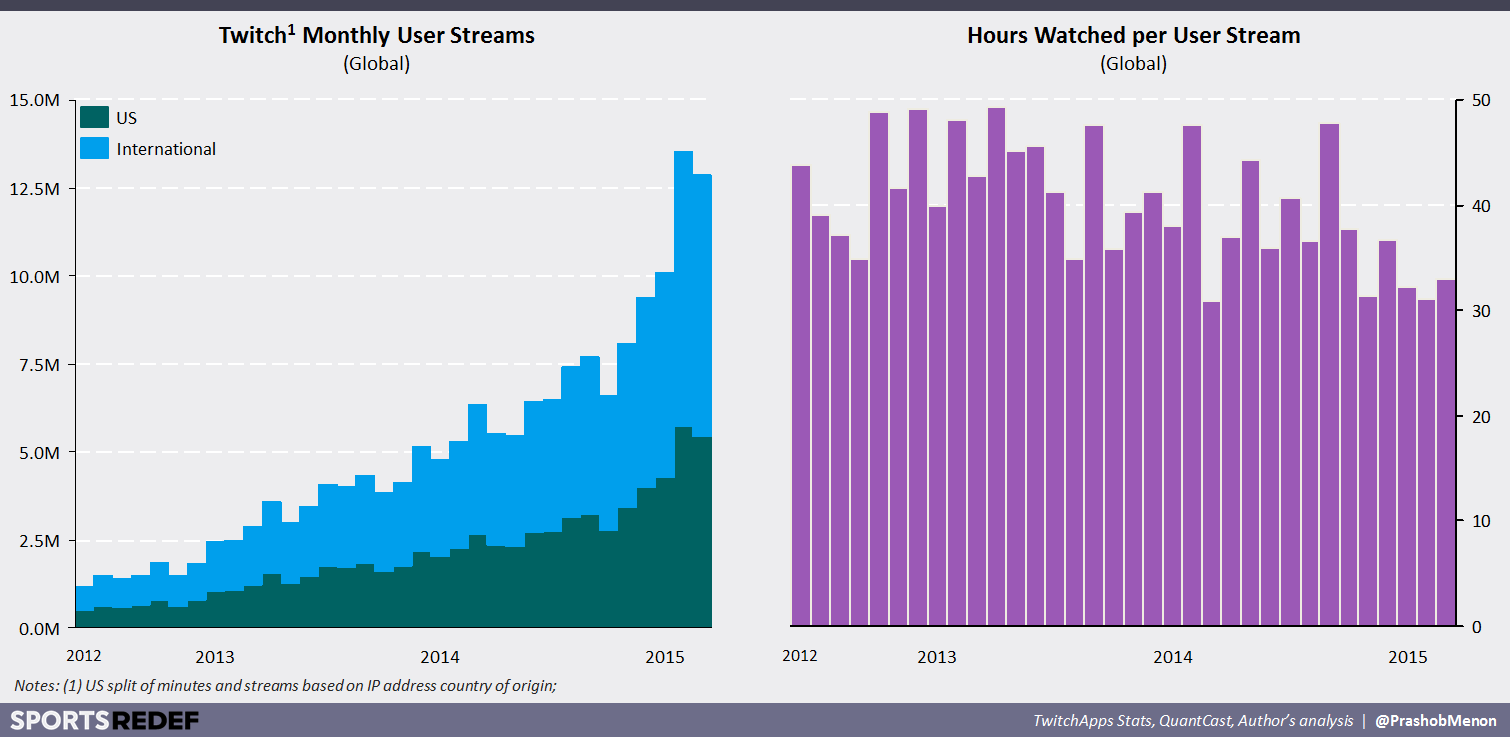

Supporting this growth is one of Twitch’s most enviable attributes: the portion of the audience involved in (cost-free) content creation. In March, more than 1.5M unique viewers live streamed their own video game feed, representing a participation rate of 3% (3x what’s typically expected online). Even more encouraging is the fact that per stream consumption has remained relatively stable even as the number of monthly streams increased tenfold.

{kind=link}

Furthermore, Twitch’s audience metrics are unlikely to stall any time soon. Despite generating $75B in revenue last year, the gaming industry is still in its global infancy:

In many ways, eSports have the potential to become the world’s first truly global sport. Even soccer, which counts 3.5B fans worldwide and is managed by a global governing body, has to contend with the logistical realities that prevent regular competition among foreign teams, as well as the fact that broadcast and cable-based distribution means most fans can only watch local games (and only if they have Pay TV subscriptions). eSports, on the other hand, are not just inherently global – they depend on connecting fans and players worldwide.

Press Enter to Start

Despite ever-growing consumer interest and potential, eSports are still far from becoming an industry. In 2014, eSports generated less than $200M in revenue worldwide, including sponsorship, advertising, licensing, ticket sales and game-publisher investment according to Newzoo. By comparison, the US-only NFL and MLB gross roughly $10 billion a year each, while the European professional soccer/football leagues generate close to $21 billion.

Even as eSports tournaments have proliferated and audiences have expanded into the millions, the value of these tournaments continues to languish. The average event offers only $18,000 in total prize winnings (a figure almost unchanged from 1998) and 2014’s 1,990 tournaments handed out a relatively unimpressive $35M collectively. The largest prize pool did surge in 2014, from $3M to $11M, but only five players made more than $1M during the year. The remaining 6,200 e-athletes took home an average of $7,000.

The disconnect between the potential and reality of eSports is not new – nor are efforts to correct this imbalance. In 2004, a group of private investors attempted to formalize an international eSports league, starting with a high-profile event called the Cyber X Games. Not only was the tournament offering $600,000 in prize money (nearly twice as large as what was then the industry’s largest prize pool), it was staged at a glamorous Las Vegas resort and received hundreds of thousands of dollars in sponsorship from the likes of ATI and AMD. Though the games picked up considerable press coverage and were attended by hundreds of players from across the globe, a combination of technical failures, denial of service attacks and poor organization led to the cancellation of all events. Players received some compensation for their expenses, but this remuneration was limited to only a portion of lodging costs, and the fate of the $600,000 in would-be winnings was never announced. As one Counter-Strike player complained, “We flew over to Las Vegas expecting a really great time. We came home tired and disillusioned.”

It was three years before the nexzt serious attempt to build a premier eSports league, with DIRECTV and News Corp. forming a partnership to launch the Championship Gaming Series (CGS). Over the following two years CGS rapidly expanded internationally, but it failed to achieve the scale necessary to thrive. After several sponsors withdrew their support, the league was closed. “Profitability was too far in the future for us to sustain operations in the interim” CGS executives said, adding “[the] economics just didn’t add up for us at this time.” A third major attempt was made by the Europe-focused Esports Global Network (ESGN) in 2013. However, the network’s linear TV-only distribution strategy and extravagant spending resulted in ESGN’s closure a year later.

Since these failures, the eSports landscape has changed in numerous ways: the costs of broadcasting equipment, software and delivery have dropped precipitously; the amount of eSports content and number of tournaments, leagues and teams have grown exponentially; tens of millions of viewers now watch live gaming feeds each week; and blue-chip advertisers have embraced the sport. Furthermore, two of the industry’s oldest (if initially less ambitious) leagues, Electronic Sports League (founded in 1997) and Major League Gaming (2002), have cultivated communities of highly engaged fans. Over time, ecosystem economics will continue to improve, but forward-thinking networks need not wait for organic growth.

Build the Business

When ESPN launched in 1978, the rights to the most popular sports in the United States were locked up by the major broadcast networks. As a result, the fledgling ESP Network (as it was known then) not only lacked the marquee events needed to attract mainstream sports fans, but its schedule was dominated by more niche (i.e. less popular) sports such as kickboxing, racquetball and volleyball. A year later, resigned to the fact that the major sports would remain out of reach for the foreseeable future, the network made an obscure but prescient bet: college sports.

In the company’s now-landmark 1979 deal, ESPN acquired the rights to rebroadcast nearly 20 National Collegiate Athletics Association (NCAA) sports nationwide. This investment served several ends. First, it allowed ESPN to fill its 24-hour programming schedule (a task which seemed preposterous at the time). Second, it ensured that ESPN could position itself as “the” network for sports fanatics – no matter the time of day or sport of choice, ESPN had something to offer. Third, and perhaps most crucially, ESPN put itself in the middle of an enormously profitable ecosystem that’s now trumpeted as an obsession by the likes of President Obama, Warren Buffett and Jeff Foxworthy.

However, this value and adoration didn’t appear suddenly – or even organically. Instead, it was the result of years of patient investment and deliberate event-building by ESPN. Here, college football is the strongest example. As the New York Times noted last year:

“[NCAA Football games are] not just televised by ESPN. They are creations of ESPN — demonstrations of the sports network’s power over college football… Every Monday morning, ESPN’s football brain trust meets to consider options for coming games and make sure the hottest teams get the choicest time slots on each of its channels. After decisions are made, calls go out across the country, setting off a scramble on dozens of campuses as universities arrange everything from parking to security to team transportation… Tickets to most games are printed with the date and the opponent’s name, but something is missing: the kickoff time. That is because ESPN, under its contracts with conferences, has the right to set kickoff times and wait until 12 days before game day, or in some cases only six, to inform universities.”

Though extreme, ESPN’s investment in the NCAA speaks to the ways in which the right partner – one that knows how to stage events, build audience and attract advertisers – could bring out the full potential of the eSports industry. There’s a widespread belief, however, that gaming is too fragmented to build a mainstream following. Yet, like physical sports, the majority of attention and value is concentrated among a much smaller set than believed.

The top five videogame franchises account for roughly two-thirds of viewership and nearly 80% of total tournament winnings. Given the 1,000+ video games released each year, this concentration is a testament to both the staying power and depth of games such as League of Legends. This trend is likely to continue as more studios focus on the handful of titles that support “gaming as a service” business models. The question, then, is who will lead the eSports charge? ESPN has already started exploring eSports by airing certain events on ESPN3 and creating a partnership with MLG, but as ESPN’s Skipper demonstrated, it may not offer the right corporate culture – nor feel the need.

Building the Next ESPN

In 2013, News Corporation announced plans to launch a new cable sports network, Fox Sports 1, in the United States. The network’s goal was simple: to steal profit share from ESPN, which captures 10% of basic cable cash flow despite representing only 2% of total viewing time. Yet even though the rookie network had the backing of one of the world’s most powerful media companies, the network faced (and still faces) many of the same challenges the independent ESPN encountered in 1978. Not only do most of ESPN’s industry-leading sports rights last until the mid-2020s (the NCAA’s Southeastern Conference extends all the way to 2034), the company has the cash flow needed to continually outbid would-be rivals – as well as the audience to do so profitably.

Though Fox Sports 1’s annual programming spend is less than one-sixth of ESPN’s, the network’s comparatively limited audience and less marketable content has resulted in significant annual cash losses. In 2014, Bernstein stimated Fox Sports 1 lost nearly $350M – while ESPN generated $2.5B. On a consolidated basis, ESPN’s six linear networks took home $3.4B versus Fox Sports 1 and Fox Sports 2’s combined $360M loss. These losses are unlikely to improve in the near future. Even when major sports become available, Fox’s sports networks will struggle to achieve the viewer scale needed to profitably acquire the rights. Rather than try to replicate ESPN today, Fox would do well to focus on emulating the sports giant’s past.

The Great Reconstruction

Though eSports have much in common with the collegiate leagues of the ’70s or X-Sports in the ’90s – a burgeoning, though still fringe interest, minimal ecosystem value and fragmented set of tournaments and conferences – it’s critical to understand the differences. eSports, unlike physical sports, represent IP, not just competition. This expands the monetization opportunities, but also intensifies the risk and complexity of the business. A war chest and organization aren’t enough to win the space.

Yet in a world of content oversupply, rising sports value and increasing Internet penetration, there are few media opportunities with the potential of eSports. A network that builds the necessary structure, stability, economics and community engagement could find itself with an empire that rivals – or even surpasses – ESPN’s.

{kind=link}

Twenty years ago, the idea of the X-Games at the Olympics seemed fantastical. Today, the sport’s ascension seems to have been inevitable. So perhaps it’s not outlandish to hear Brandon Beck, CEO of Riot Games, say that “eSports will be part of the Olympic Games” during his lifetime. Whether or not eSports are “real” sports fundamentally misses the point – what matters is that even today they draw huge audiences who are passionately engaged in the content. Caring for both sides – the business and the culture – will be the defining trait of whoever wins the space. Doing so won’t be easy, but building an empire never is.

Prashob Menon is a Strategy Consultant in the Technology, Media & Telecommunications sector. He can be reached at menon.prashob@gmail.com or on Twitter.

Matthew Ball is a Director of Strategy & Business Development at Otter Media and leads Strategy & Originals at REDEF.