Credit: TT News Agency / AlamyDaniel Ek admitted personal responsibility for Spotify's over-spending vs. revenue generation this week, which led to over 500 job cuts

MBW Reacts is a series of analytical commentaries from Music Business Worldwide written in response to major recent entertainment events or news stories. Only MBW+ subscribers have unlimited access to these articles.

“I take full accountability for the moves that got us here today.” And so he should.

Daniel Ek‘s admission that he bears personal responsibility for yesterday’s news of Spotify cutting over 500 jobs is noble. It’s also 100% justified.

In my view, Ek’s loss-making company has played with fire on three key matters these past few years:

(i) Spending a monstrous amount of money on staff, sales, and marketing;

(ii) Spending a monstrous amount of money on Spotify’s podcasting strategy, despite podcasting burning through Spotify’s funds; and

(ii) Stubbornly refusing to increase the price of Spotify’s flagship subscription service in its biggest market – not even once – over the past 12 years. Despite the fact that doing so would have likely made Spotify… a monstrous amount of revenue.

These three factors have coalesced to squeeze Spotify’s gross margin figure, which missed the company’s own guidance in Q3 2022.

This gross margin struggle has sent Wall Street analysts into a flap these past few months, and ultimately contributed to Ek’s decision this week to cut 6% of Spotify’s global workforce.

Factor 1) Spending a monstrous amount of money on staff, sales, and marketing.

At this point it’s worth examining Daniel Ek’s own words, from an internal letter sent yesterday to Spotify staff.

In his reasoning for cutting 6% of Spotify’s global workforce, Ek wrote: “In 2022, the growth of Spotify’s [operating expense] outpaced our revenue growth by 2X. That would have been unsustainable long-term in any climate, but with a challenging macro environment, it would be even more difficult to close the gap.”

Added Ek: “In hindsight, I was too ambitious in investing ahead of our revenue growth.”

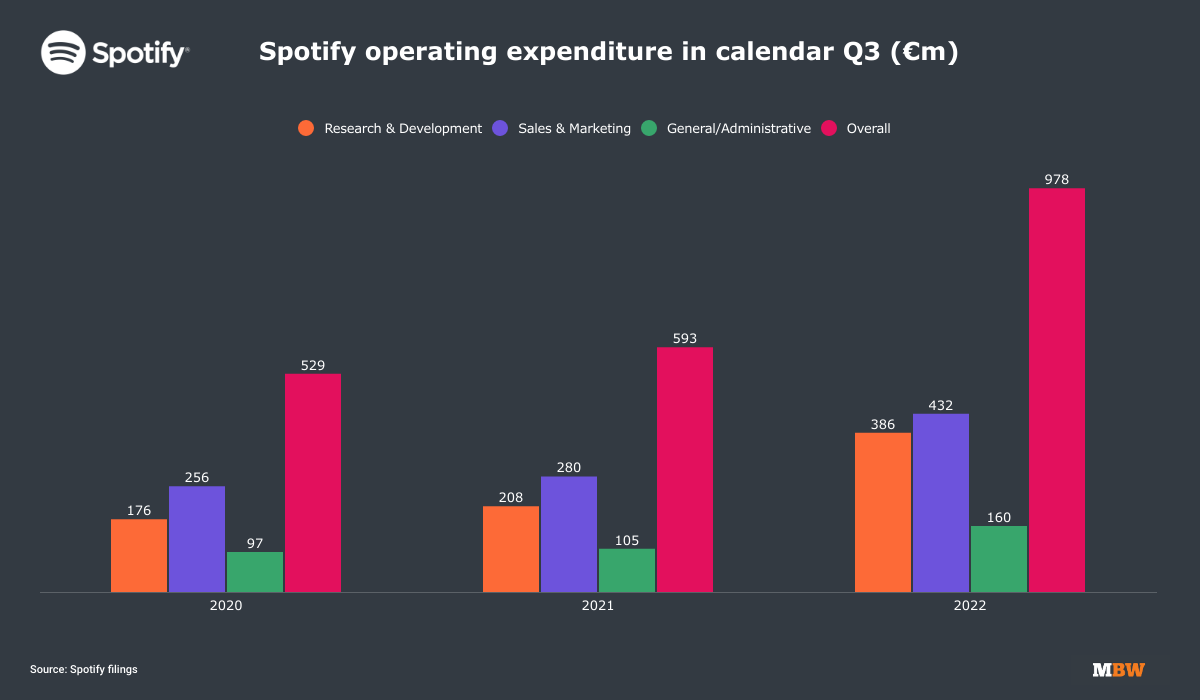

In that article, published earlier this month, we noted the following: “Q3 2022 was a milestone quarter for Spotify, which spent comfortably over USD $1 billion on operating costs [in the three months].”

In fact, Spotify’s operating costs in Q3 2022 (EUR €978m) were nearly double the size of its operating costs in the prior-year quarter (€593m, see chart below). Ek’s “too ambitious” quote rings in the ears.

SPOT’s huge USD $1 billion+ Q3 2022 operating cost burden actually swallowed up around a third of its total revenues (EUR €3.04 billion) that quarter.

As pointed out in MBW’s ‘5 numbers’ piece, these stats clearly put paid to the fallacy that “the record companies are eating up all of Spotify’s profits”.

Specifically, nearly half of Spotify’s USD $1 billion+ spend on operating costs in Q3 2022 (€432m, or close to half a billion dollars) went on sales and marketing.

Spotify’s operating expenditure in Q3 2022 was nearly double the size of its operating expenditure in Q3 2021

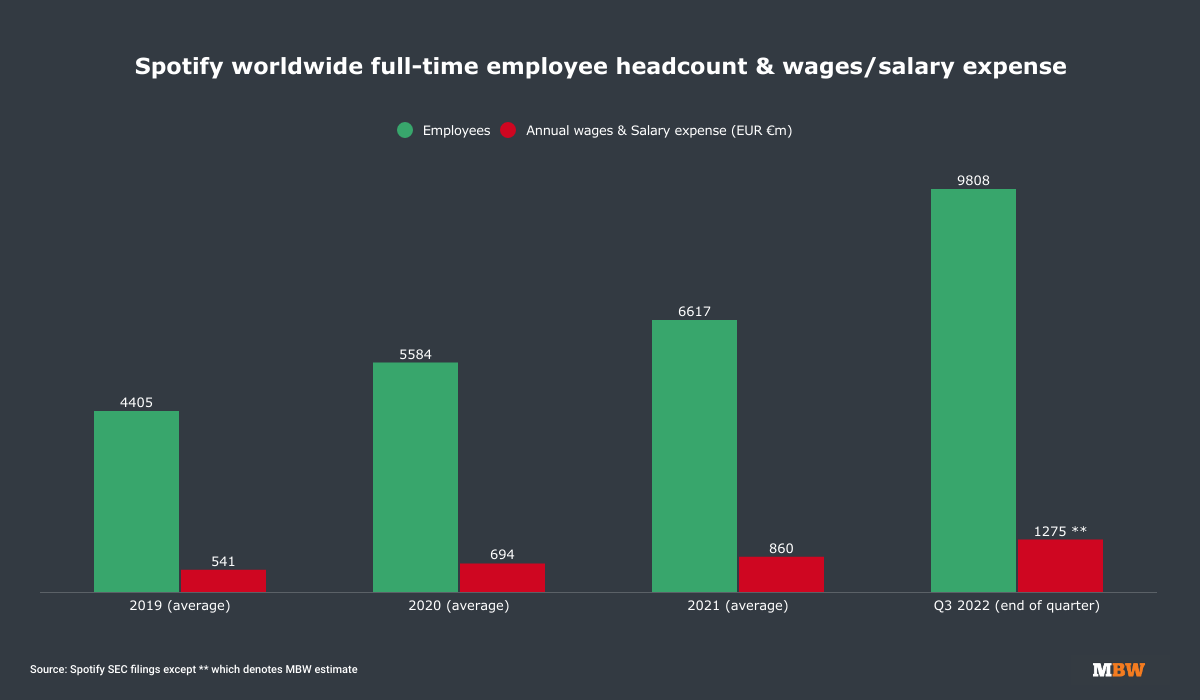

Now let’s look at the other big drain on Spotify’s operating expenses: people.

During 2021, according to its latest annual fiscal report, Spotify employed 6,617 people on average, an increase of over 1,000 employees per year.

The company spent EUR €860 million (USD $1.016 billion) on the wages and salaries of those 6,617 employees in 2021, according to a Spotify SEC filing.

Ergo: the average annual salary at Spotify during 2021 was approximately USD $153,543.

By the end of Q3 2022, Spotify’s full-time employee count had mushroomed to a whopping 9,808 people according to a SPOT presentation for investors, up by around 3,000 employees across just the prior nine months.

(To put that Q3 2022 employee number into music biz context: 9,808 figure is more employees than Universal Music Group – the world’s biggest music rightsholder – counted at the close of 2021 at 9,505.)

We don’t have a figure for the total wages/salary cost absorbed by those 9,808 Spotify employees in Q3 last year (Spotify only includes wages/salary data in its annual reports for the full year).

But if the average yearly wage of a Spotify employee from 2021 (USD $153,543) still held true in September last year, then by this point Spotify would have been looking at an annual salary bill just north of EUR €1.2 billion /USD$1.5 billion.

A $1.5 billion annual wage bill. For a loss-making company. Which had just failed to hit its own gross profit margin guidance. And was spending over $1 billion a quarter (!) on operating expenses.

Something had to give.

Note: Q3 2033 annual wage figure is an MBW estimate based on 2021 average employee salary

Factor 2) Spending a monstrous amount of money on Spotify’s podcasting strategy, despite podcasting burning through Spotify’s funds

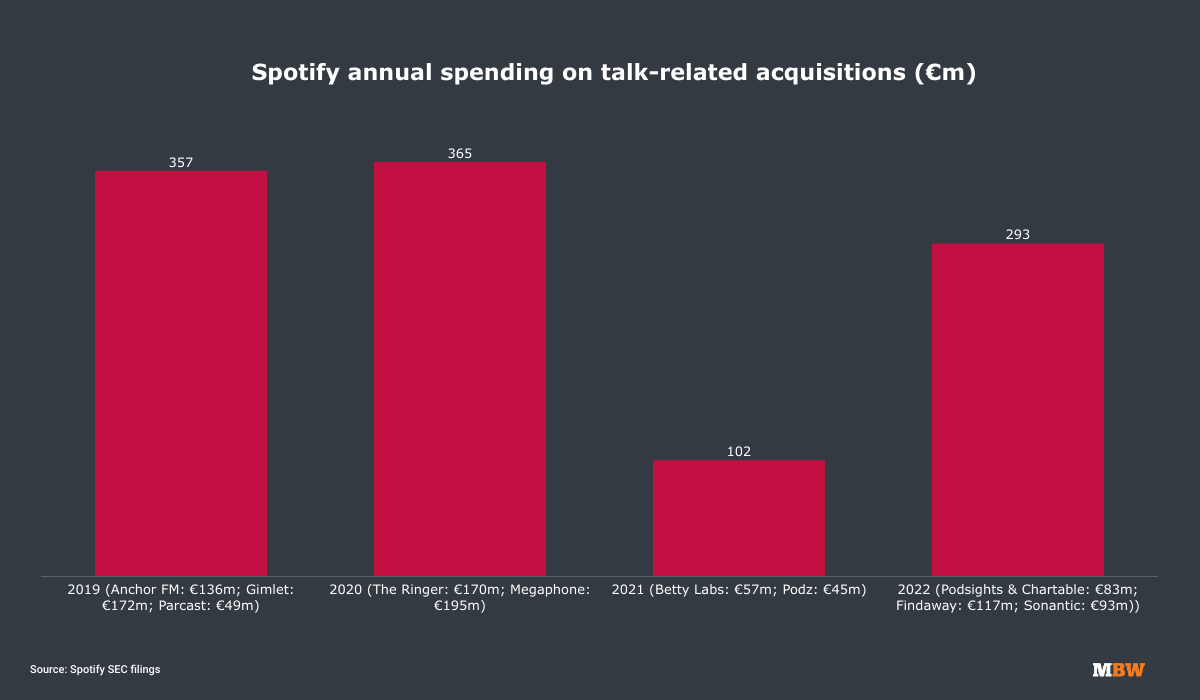

One way that Daniel Ek has quickly fattened up the wage bill of his company is via acquisitions, in one particular area: Podcasting and talk content.

Ek’s preoccupation with Spotify’s non-music business has seen his company spend EUR €1.11 billion (around USD $1.2bn) on talk-focused acquisitions over the past four years (see chart below).

Some of those acquisitions look smarter than others today: Spotify’s €117 million acquisition of audiobook service Findaway in 2022, for example, has thrust Ek’s company into a lucrative digital market (with an established paid-for model) currently dominated by Amazon‘s Audible.

Others of Ek’s massive-money bets appear less… prudent.

May we remind you that in 2021, in the middle of the pandemic, Spotify spent over USD $60 million on Betty Labs (Locker Room) – a live audio rival to the then-app-of-the-moment, Clubhouse.

Huh? What do you mean you don’t remember Clubhouse?!

The biggest area of acquisitive spending for Spotify throughout the past half-decade, however, has specifically been in podcasting.

From 2019 through 2022, SPOT spent EUR €850 million (around $925m) on acquiring multiple platforms to drive Spotify’s podcasting business – from Parcast to The Ringer, Anchor FM, and, most recently, Podz, Podsights and Chartable.

That $925 million figure doesn’t count the cash Spotify spent on non-acquisitive Podcast content deals: For one thing, we know it spent at least another $200 million on a multi-year exclusive deal for the Joe Rogan Experience. Spotify also spent further vast sums on podcast content from the Obamas, Kim Kardashian, and Harry and Meghan, amongst others. (Not all of these deals have worked out.)

So, financially speaking, what’s Spotify got to show for four years and over a billion dollars in podcast investments?

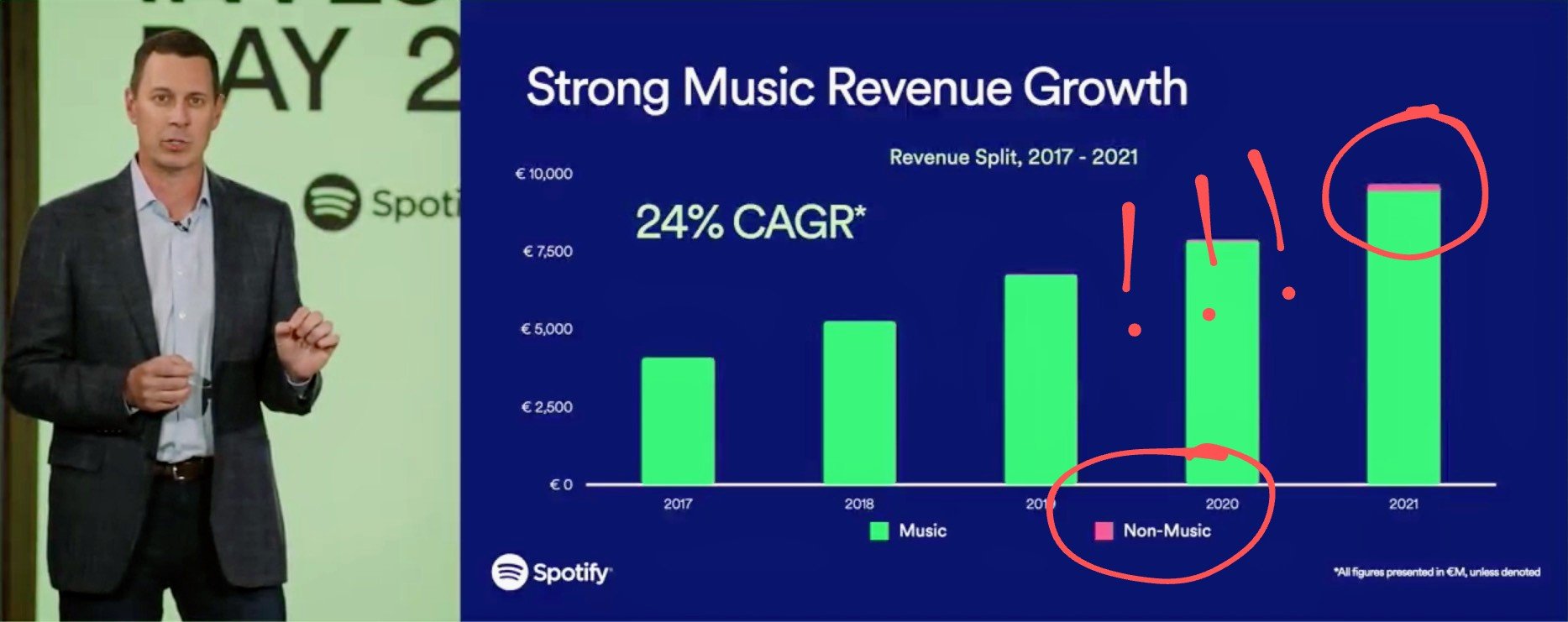

According to an Investor Day presentation by senior Spotify leaders in June last year, the firm’s podcasting efforts generated under €200 million in advertising in 2021.

If you were wondering how that compares to the amount of money generated by music (via subscriptions and ads) on Spotify in the same 12 months, I recommend you look at this single image, of Spotify CFO Paul Vogel, from that summer 2022 investor presentation.

The green bit is music-related revenue in each year

The gaunt wisp of pink at the top of the last bar? That’s revenue from everything else – including podcasts. (Digital graffiti, author’s own.)

There were, though, grand proclamations at that June 2022 investor presentation about the riches that awaited Spotify for its heavy investment into podcasting.

Daniel Ek predicted that podcasting, although it was “not yet profitable”, had a “40-50% gross margin potential” in the future.

Paul Vogel then revealed precisely how “not yet profitable” podcasting was.

He confirmed that Spotify’s annual podcasting revenue grew by “more than 300%” to “nearly €200 million” in 2021, before adding: “However, this growth came with a €103 million negative impact on gross profit.”

A “negative impact on gross profit”, if you were wondering, is coddling finance speak for a big, fat, annual loss.

Vogel then admitted that 2022 would see a more severe “negative impact” on gross margins from podcasting at Spotify (i.e. an even bigger, fatter annual loss). But he forecast that podcasts would “turn profitable over the next 1-2 years [after that], with a meaningful ramp from that point onward”.

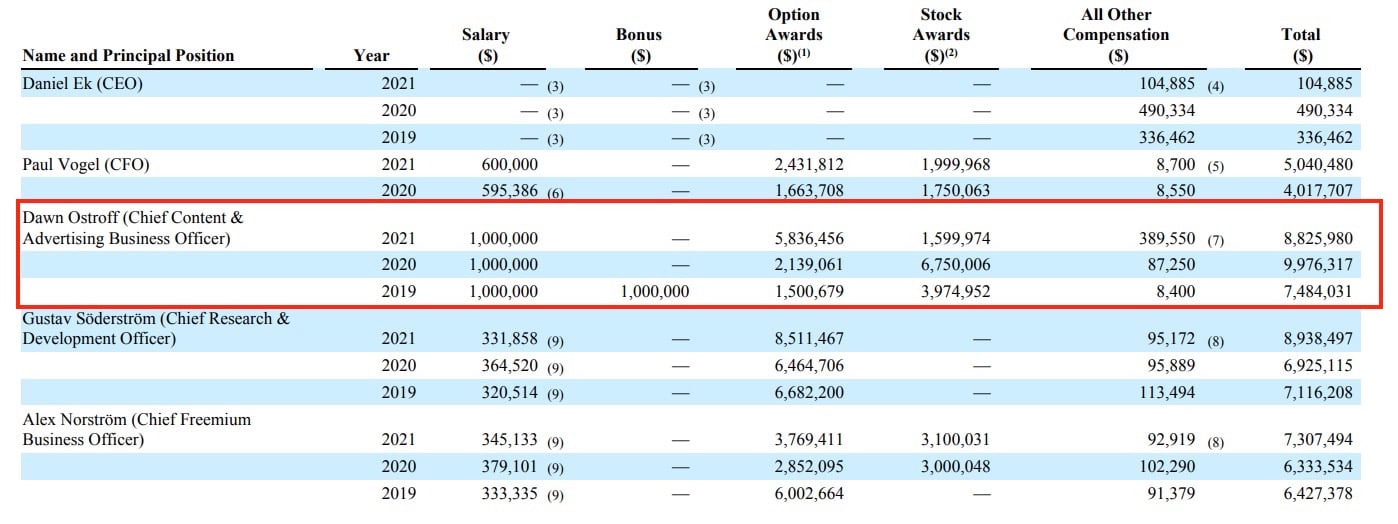

The most bullish person about podcasting on that July investor showcase, though, was Dawn Ostroff.

Spotify’s Chief Content and Ad Business Officer, who joined the firm in 2018, suggested: “We see podcasts becoming a $20 billion global opportunity by 2030.”

“We see podcasts becoming a $20 billion global opportunity by 2030.”

Dawn Ostroff, Spotify, speaking in June 2022

Time will tell on all of these glowing predictions – but Ostroff won’t be at Spotify to see if her words ring true.

Alongside its announcement that 500 people were being laid off yesterday, Spotify confirmed that Ostroff – who has been responsible for making hundreds of millions of dollars in investments in ‘exclusive’ and ‘original’ podcasts – was exiting her role at SPOT.

Ostroff, whose duties have now been taken up by existing management at Spotify (mainly Alex Norström), pulled in a total annual executive compensation package of USD$8.83 million in 2021, according to Spotify filings, and USD$9.98 million in 2020 (see below), with a $1 million base salary in each year.

As such, Ostroff’s departure is likely to result in a significant operating expense saving for Spotify of its own accord.

Factor 3) Stubbornly refusing to increase the price of Spotify’s flagship subscription service in its biggest markets

I remain flabbergasted at the easy ride Daniel Ek has been given from Wall Street analysts in the past few years on this one.

Let’s remind ourselves: According to World Bank/OECD data, when Spotify launched in the United States in 2011, the country’s annual GDP – widely accepted as the leading economic indicator for any nation – stood at USD$15.6 trillion.

By 2019, a year before the pandemic sent economic certainties shuddering and spiraling, that annual GDP figure had grown to USD$21.38 trillion. Unemployment in the States fell to historic lows in the same period.

The ‘twenty-tens’ were an economic boom period so good, then-President Donald Trump (remember him? You’ve got to admit: more memorable than Clubhouse) claimed, with typical self-effacement, that his administration had “built the greatest economy in the history of the world”.

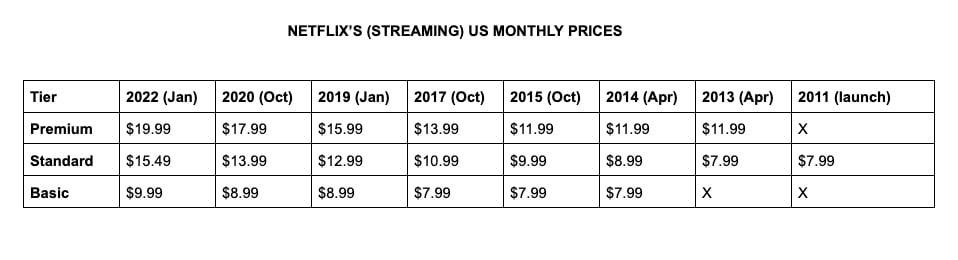

Guess how many times Spotify raised its prices in the world’s largest music market amid this decade of extreme economic plenty? Zero. Zero times.

Guess how many times Netflix raised its US prices during the same period? Four. And then twice more, once in 2020, and once in 2022.

In fact, Netflix’s Standard-tier monthly price in the US is now nearly double the size of what it cost back in 2011 ($15.49 vs. $7.99, see below).

For a moment there, in early 2022, when Putin launched his despicable war in Ukraine and the globe’s macroeconomics started to crumble, this all came back to bite Netflix on the downstairs cheeks.

You might remember that in April last year, Netflix announced it had lost around 200,000 net subs globally. Things got worse: In its Q2 results, Netflix announced it had lost another million-ish subscribers.

The world, MBW included, jumped to the same conclusion: Too many price rises had hurt Netflix, and cash-aware subscribers, with a recession on the way, were fleeing in their droves.

In the wake of Netflix’s H1 2022 woes, Daniel Ek didn’t waste the opportunity to frame his company’s inaction over US price rises in the prior decade as a masterstroke.

In June 2022, discussing Spotify’s historical lack of movement on flagship price rises, Ek told investors during a Q&A: “I personally look at what’s happened in the video streaming business and I wonder to myself if that industry didn’t get ahead of itself.

“Because frankly, yes, it did increase prices, but it’s also now finding itself in a position where it’s harder and harder to find future growth.”

Aka: Me smart; Reed Hastings dumb.

Yeah, that little narrative didn’t last long.

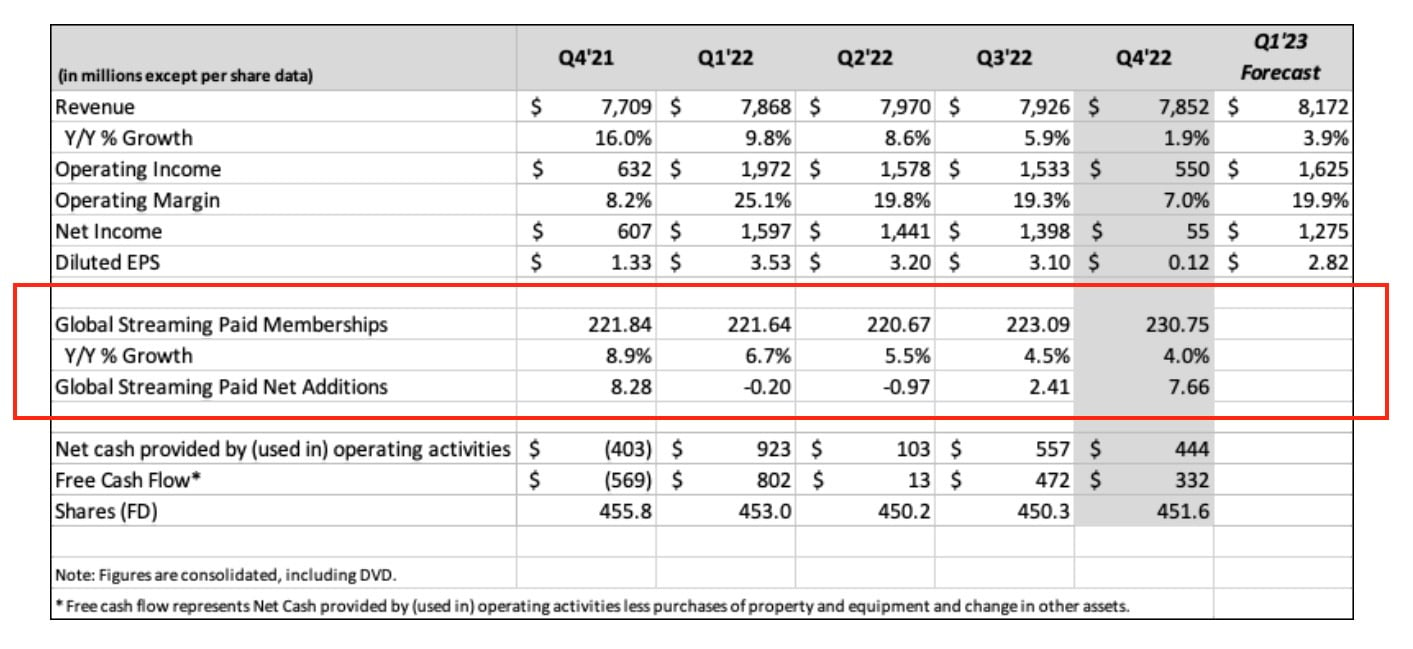

In Q3 2022 – in what we’ll term its ‘recovery quarter’ – Netflix added 2.42 million paid subscribers (see below).

And in Q4 2022, as it announced just the other day – in what we’ll term its ‘smashed it out the park’ quarter – Netflix added another 7.66 million paid subscribers.

Despite its Premium tier costing double the price of a Spotify Premium subscription, Netflix had roared back to health.

All of this came off the back of a very successful pandemic for Netflix, in which it added 18.18 million paying subs in FY2021, and 36.57 million subs in 2020.

Source: Netflix letter to shareholders, Jan 2023

The argument often made against Spotify raising its prices a la Netflix is this: Music streaming is a different beast to film streaming, because the major record companies ensure that no single streaming service has the uniqueness of content – especially original content – that Netflix does. And that uniqueness of content is vital to secure customer loyalty vs. rival services, even through price rises.

Indeed, trying to secure that exact kind of exclusive content is largely what’s been driving Spotify’s recent mega-spending on podcasts (that I’ve spent a fair chunk of this column critiquing).

Both fair points.

But there’s a counterargument, too: May I remind you that Spotify itself suggests to its investors that its algorithmic recommendation engine is special enough to create unique customer loyalty in the music streaming space. “Spotify is more than an audio streaming service,” it boasts in its SEC filings. “We are in the discovery business.”

It adds: “Every day, fans from around the world trust our brand to guide them to music, podcasts, and entertainment that they would never have discovered on their own. If discovery drives delight, and delight drives engagement, and engagement drives discovery, we believe Spotify wins and so do our users.”

Regardless, despite the undoubted lobbying of the major record companies (plus Merlin and co), Spotify held firm on not raising prices throughout a decade (2011-2019) when the US economy was solid as granite.

Spotify also balked at raising its US prices during a pandemic (2020-2021) that resulted in media streaming services – SPOT and Netflix included – seeing some of the most successful subscriber growth in their histories.

Spotify has raised some prices globally in the past two years: Most have affected family/student/Duo-type bundles, but the standard individual Spotify Premium price has itself been pushed up in recent times, for example, in Brazil, Sweden, and Norway.

The financial impact of these price rises for SPOT (Daniel Ek claims there were 46 separate rises around the world in total during 2020-2022) has been dramatic. The evidence:

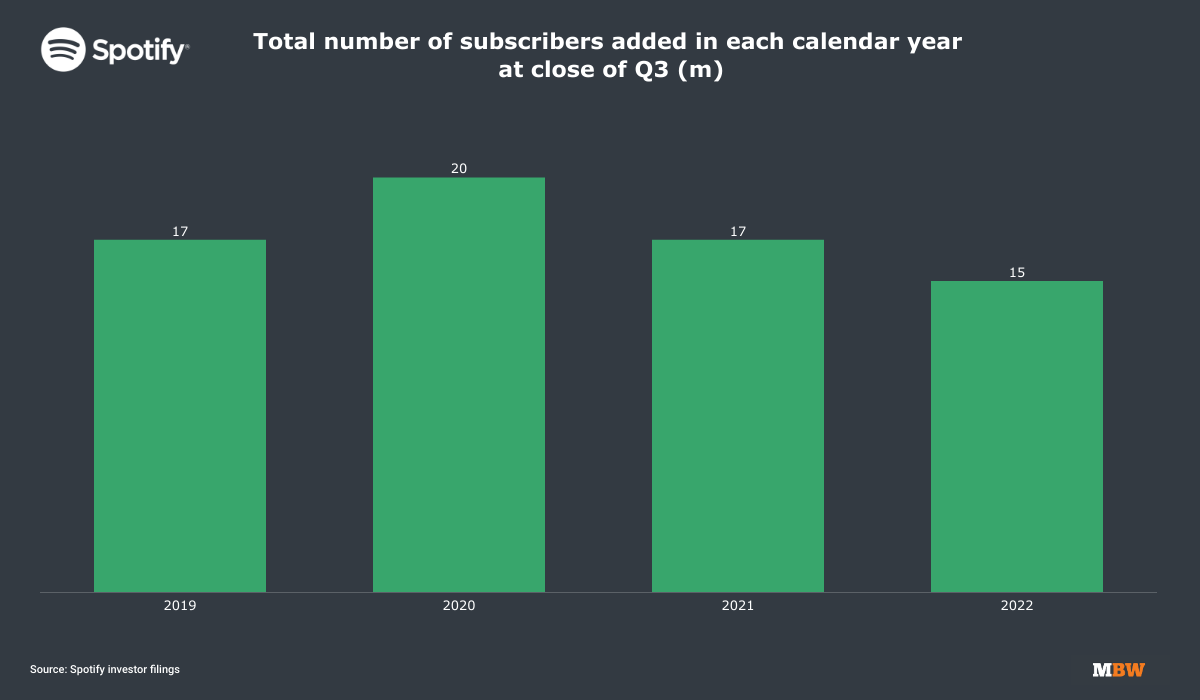

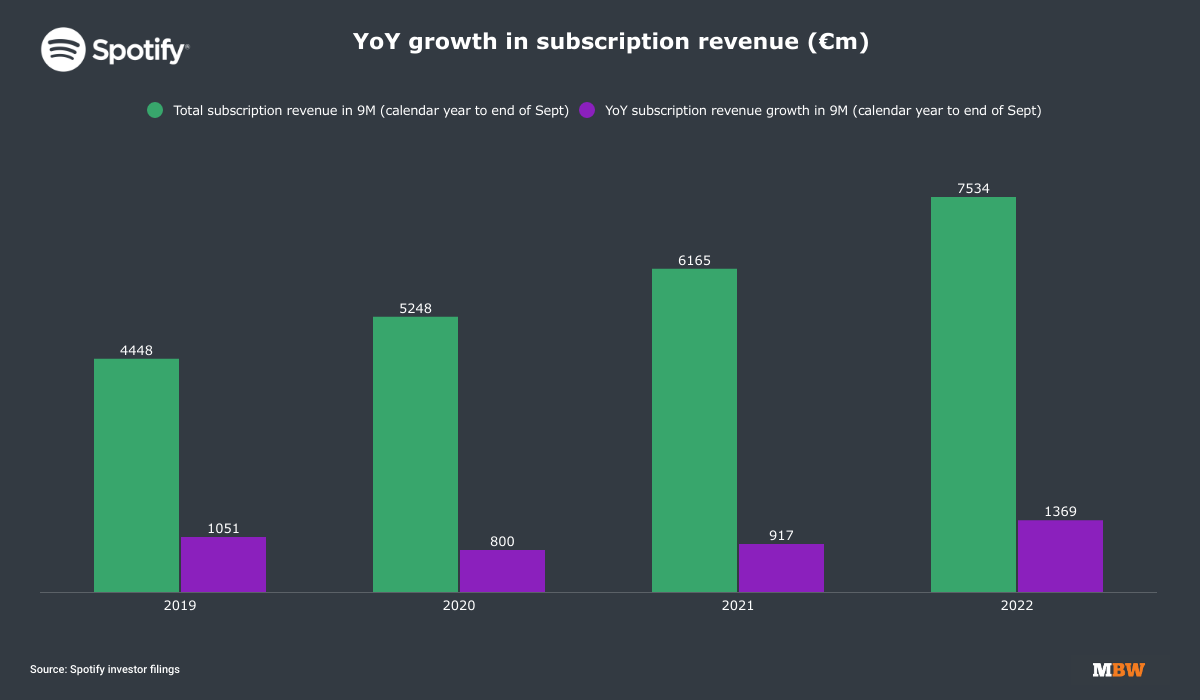

Spotify saw smaller YoY growth in total volume of global subscribers in the first nine months of 2022 than it did in the same period of 2021 (15m vs. 17m, chart No.1 below);

But in terms of subscriber revenue growth, partly thanks to those price rises, Spotify saw its biggest ever YoY increase (+€1.37bn) in the same nine-month period (Jan-Sept, chart No.2 below).

Clearly, maturing streaming markets have been able to bear price increases from Spotify; swathes of subscribers didn’t disappear from the service in disgust.

Yet mysteriously, in the world’s biggest music market, the United States, Spotify’s flagship Premium offering has remained stuck at that $9.99 price point for 12 long years.

Even now, in 2023, after Amazon Music and Apple Music have both hiked their standard individual streaming prices in the States, Spotify continues to refuse to do so.

And that’s not even mentioning inflation: According to CPI data, Spotify would now have to charge $13.00 per month for its Premium service in the US for its price-tag just to be worth the same, in real economic terms, as the $9.99 it charged in 2011.

Spotify had 195 million paying subscribers at the end of Q3 2022, of which around 55 million were located in North America, according to SPOT’s investor filings.

Had Spotify, at some point over the past decade, been able to raise the average spend of those North American subscribers by just USD $1 per month, it would now be generating $660 million more in revenue per year.

Had it been able to raise the average spend of those same North American subscribers by USD $2 per month – perhaps, shock horror, via two price rises across the course of a decade-plus – it would now be generating over $1.3 billion more a year in topline revenue.

Yes, most of that revenue (≈70%) would have to be shoveled back out to music rightsholders in royalties. But it would have provided Daniel Ek the cover he needed to overspend on podcasts in that crucial 2019-2022 period – firm in his belief, as he is, that this podcast investment will ‘come good’ eventually.

Instead, Spotify has wimped out of raising its US pricing in the past 12 years, even as Netflix has braved doing so multiple times over.

As a result, that revenue cover isn’t there, Spotify is cutting over 500 jobs, and Daniel Ek’s admitting it’s all his fault (without, notably, actually saying sorry to his staff or his investors).

The colossal expenditure Spotify has thrown at podcasts – combined with the lack of revenue growth needed to prop up its gross margin – reminds me of this line within the company’s ‘risk factors’, printed in its annual report each year.

“We have made, and expect to continue to make, significant investments to develop and launch new products, services, and initiatives, which may involve significant risks and uncertainties, including the fact that such offerings may not be commercially viable for an indefinite period of time or at all, or may not result in adequate return of capital on our investments.”

It’s right there in black and white. “[M]ay not be commercially viable for an indefinite period of time… or at all”.

No one can say they weren’t warned.Music Business Worldwide